Mortgage Blog

Canada's Mortgage Experts

Bank of Canada Holds Rates - What Now?

September 8, 2023 | Posted by: Mortgage Bridge Canada

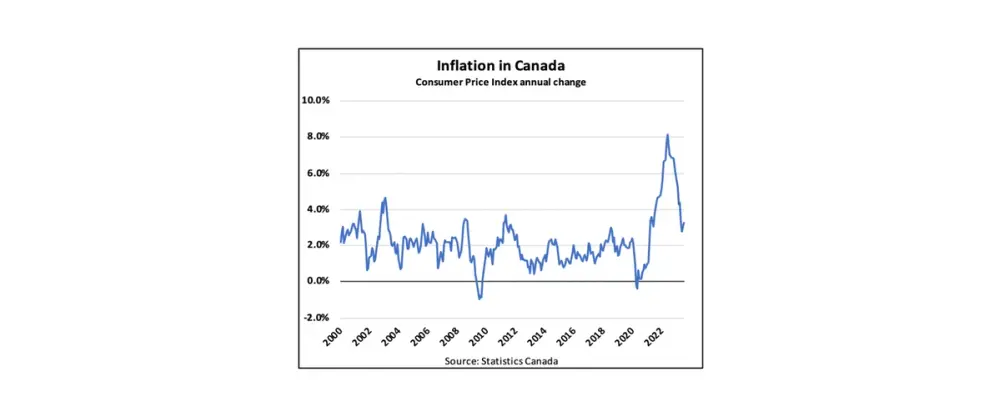

Good news! The Bank of Canada has paused their interest rate hikes as inflation has become more under control, but will it be the last? Many economists think so as we are closing in on their target inflation rate of 2% and there are many indicators that signal we are on the right path. So, what does this mean for interest rates? Here are the impacts and options ahead:

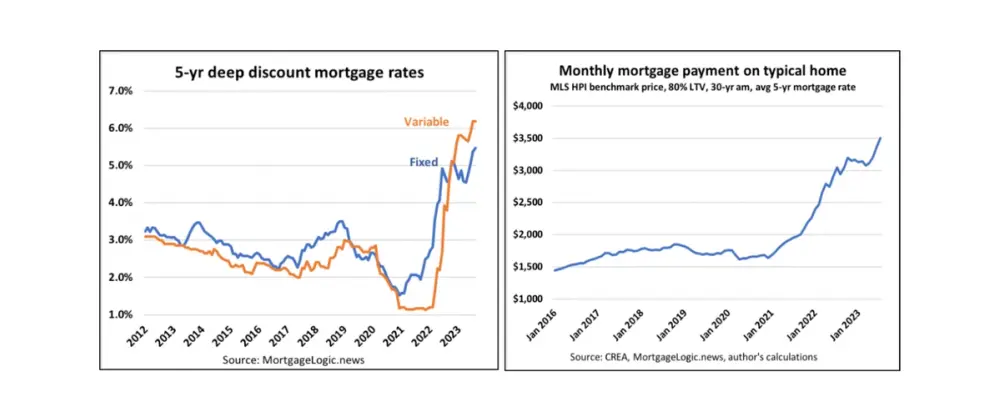

Variable - The prime rate for variable and adjustable-rate mortgages, HELOCs and credit cards, will stay the same. Meaning, for existing variable rate mortgage clients your mortgage payments won’t change. However, for new variable rate mortgage clients, interest rates the lenders offer may start to come down in response to the hold.

Fixed - Although not pegged to the Bank of Canada key policy rate, fixed-rate mortgages might also start to come down slightly over the next few weeks. Considering the fixed rates have nearly doubled in the last year to over 5%, this is great news.

Should you wait to purchase, sell, refinance or renew your mortgage?

Any decrease in rates will likely be small at this time. The majority of bank lenders predict that it will take until mid-year 2024 for the Bank of Canada to start dropping their rates. And once this occurs, it will still take time for the lenders’ rates to move down into the 4% range. However, that doesn’t mean there are no opportunities today to purchase a new property, get a better-rate mortgage, or renew at a rate that allows you to maintain your cash flow or financial plans. That’s where we can help.

How Will This Impact Homeowners?

Higher mortgage rates at renewal. Many homeowners approaching their mortgage renewal date in the next 18 months may face higher mortgage rates. Variable mortgage rates have increased from the low 1% range to 6% range, while fixed rates have increased from the mid-2% range to 5% range. So, it is important for homeowners to reach out to their mortgage broker to discuss how their monthly payment or mortgage qualification might change and the options available to obtain the lowest rates in the near future.

- Renewals on Fixed (5.25%):

- 2018 - +2.25%

- 2019 - +2.75%

- 2020 - +3.25%

- 2021 - +3.50%

- Renewals on Variable (Prime -0.90% at 6.3%)

- 2018 - +4.00%

- 2019 - +3.00%

- 2020 - +4.00%

- 2021 - +5.00%

Payments stabilize. Borrowers with adjustable rate mortgages (ARM) will not see another increase in their mortgage payment this month. If you are struggling to make these payments, there are solutions available such as debt consolidation, refinance, or moving to a lender with a lower rate to help ease the strain of borrowing costs.

How Will This Impact Home Buyers?

The stress test today is the lender's “contract rate plus 2%”, which has pushed the minimum qualification rate for prime mortgages into an average of 7 to 8% and alternative mortgages closer to 9%. A small reduction in interest rates from lenders can help improve your chances of getting into the market this fall. There are many strategies to help improve your purchasing power, obtain a lower rate, and qualify, including co-signing, gifted down payment support, porting the mortgage to a new home to get a lower blended rate, and qualifying at the lender “contract rate” vs. “contract plus 2%”.

How Will This Impact Investors?

BoC rate hikes over the past year have increased the cost of borrowing and lowered the cash flow potential for investors in most markets. As rates stabilize and lower, more opportunities will become available to improve the health of investor's portfolios. And the good news is there are already solutions and opportunities out there today to help investors stay on track including extended rate holds on pre-construction, higher Loan-to-value allowances and specialty renovation loans that won’t put a strain on savings accounts.

Pineapple brokers can help you find solutions to improve your financial health and help you navigate through market changes. Contact your Pineapple broker today to get a clear understanding of how the Bank of Canada rate holds and how future rate declines will impact your financial future.